Space for Earthlings

The Impact of Space Operations on Modern Business: A Guide for Leaders

- •Captivating stories about space-faring species traveling the galaxy make for appetizing entertainment, but they belie the substantial capabilities of the Space industry.

- •These capabilities are enabling for business leaders of traditional industries here on Earth.

- •‘Earthling’ industrial sectors face shared day-to-day challenges of running organizations, maintaining employees, sustaining supply chains, and a myriad of other executive priorities.

The Space industry is expanding beyond exploration. From logistics to agriculture, communications to risk management, business activities on Earth will be increasingly influenced by activities occurring in Space. This Enhanced & Expanded edition features interactive frameworks, a self-assessment tool, updated 2026 data, and deep cross-references — a guide for business leaders in traditional industries who want to understand how Space capabilities are reshaping the competitive landscape.

Foundation

We are all Earthlings

We are all Earthlings

Captivating stories about space-faring species traveling the galaxy make for appetizing entertainment, but they belie the substantial capabilities of the Space industry. These capabilities are enabling for business leaders of traditional industries here on Earth. ‘Earthling’ industrial sectors face shared day-to-day challenges of running organizations, maintaining employees, sustaining supply chains, and a myriad of other executive priorities.

This collection of articles focuses on what is important for senior business leaders outside of the space industry to be aware of, to evaluate, and to anticipate what new capabilities and price-points may be feasible in the coming years. Grounded with a plethora of illustrative case examples looking retrospectively and prospectively, readers will develop a better sense of notable areas of progress associated with the Space industry and its growing impact across multiple sectors. Furthermore, a practical guide is included for business leaders to self-assess relevance of various Space indicators to the upcoming needs of their organizations.

First, a synopsis of terminology specific to this collection of articles: “Earthling” and “the Space industry”.

The label “Earthling” is intended to refer specifically to someone who is focused on running their companies, institutions, and other organizations, and are overall prioritizing getting on with life right here at home.[1, 2]

What is ‘the Space industry’? It’s all of the economic activities and services associated with craft that are located sufficiently high above our planet’s surface, about 100 kilometers (60 miles), higher than the routes of all aircraft. The Space industry is broad, encompassing satellite communications, Earth observation, global navigation and positioning, launch services, and a variety of emerging areas. These include Space-based mining, tourism, war, cybersecurity, and manufacturing.

[1] For those individuals whose main focus is to look beyond our planet, they are still Earthlings, of course, but are more likely to already be Space-informed, and are thus not the primary audience for these articles.

[2] We are not currently delving into Unexplained Anomalous Phenomena and Non-Human Intelligence.

Foundation

What is going on up there?

What is going on up there?

Space is no longer just the playground of the stars, whether of the celestial or celebrity variety. The Space industry is expanding its focus beyond ‘Space exploration’. From logistics to agriculture, communications, privacy, to risk management and competitive intelligence, business activities on Earth will be increasingly influenced by activities occurring in Space. The industry is diversifying. Its sources of investment from solely the realm of well-funded nation-states is now enjoying an influx of capital from private sources. Additionally, the Space industry is maturing beyond the “New Space” hype of the late 2010s/early 2020s into the emergence of Space-capable organizations that are prioritizing their focus on benefiting all of us. Business leaders would be wise to understand what new capabilities are becoming feasible that were previously only part of science fiction or for billion-dollar budgets. Likewise for government agencies, the commercial era of Space is necessitating changes to their strategies, too, as a February 2024 report from BCG details.

Newly-accessible capabilities such as earth sensing and imagery, zero-gravity manufacturing, new pharmaceuticals, and industrial mineral extraction are beginning to influence how we do things here on Earth.

When you view a map on your smartphone, the blue dot marking your current location is the result of billions of dollars of space infrastructure. “Sure it results in food delivery, dating apps and so many innovations in daily life, but none of this would be possible without the boundaries of exploration into space,” says Van Espahbodi, managing partner and co-founder of Starburst. It is unfeasible to lay copper or fiber optic cables over every mountain, under every sea, and certainly not possible to tether airplanes, automobiles, or most maritime vessels. For the billions of people globally who are beyond the physical reach of hardwired Internet connections, “you have no choice but to drop internet beams from space,” says Felix Ejeckam, CEO and founder of Akash Systems.

For example, few of us use expensive satellite phones that have existed for decades, but many of us expect nearly-globally-accessible broadband Internet connectivity. SpaceX’s Starlink service is rapidly establishing itself as critical communications infrastructure, with public awareness increasing due to its role in hotspots of global conflict and in providing accessibility in cool spots beyond “the last mile” of traditional terrestrial Internet providers. In fact, most of these articles were composed while connected to a consumer-grade Starlink terminal in the Allegheny Mountains of Pennsylvania.

Another example of a newly-accessible capability is having a manufacturing facility in a sustained low-gravity environment. Sounding rockets have provided us with an ability to conduct, short-lived, low-gravity experiments, but the drastic reduction in launch cost and increase in performance of small satellites is enabling terrestrial companies to develop new forms of pharmaceuticals (e.g., Varda Space Industries), synthetic biology (e.g., Yuri Gravity), and other health and living systems in sustained microgravity and zero gravity environments. The return of these grown and manufactured substances back to earth can enable new life science applications that were previously infeasible and nearly unimaginable. If a leader of a pharmaceutical company is not tracking how to conduct zero-gravity operations, the leader may find the organization at a significant disadvantage as the industry begins to see a step-up in off-planet manufacturing capability. The possibility of an entirely new class of ‘Space-enabled’ drugs, both biologic and small molecule, could uncork huge areas of market growth.

The Space Industry’s rapid expansion means change, which is potentially lucrative for those who pay attention and devastating for those who ignore.

Foundation

How to think about new Space capabilities

How to think about new Space capabilities

In years past, a Space-curious organization would expect to build most of its own capabilities,literally assembling the nuts and bolts of satellites, securing a spot on a rocket a couple years in advance, and handling all manner of other collateral work to get stuff into Space and to then retrieve data or objects from Space. This is incredibly expensive – at least several hundreds of millions of dollars. But that is no longer the situation.

For an organization to develop a Space capability, there are launch services such as SpaceX which provides the “cargo ship” that accommodates “shipping containers,” satellite platforms such as Rocket Labs’s** Photon** satellite bus with standard components such as solar panels, battery, primary radio, and other balance-of-plant. This is a recent phenomenon developed over the past decade that now enables Space-curious organizations to focus on their unique area of value creation, such as Varda’s pharmaceutical factory and reëntry pod. [1] SpaceX has built a business platform upon which other businesses (including startups and new-to-Space companies) can develop new product-services.

Since most organizations no longer need to control the majority of their own Space equipment, executives can look at what new Space-based capabilities are coming online, and which others are becoming available at lower cost and higher fidelity. Prepared below is a capabilities chart to aid Earthlings. We call it the S.P.A.C.E chart (Strategic Potential for Advanced Capabilities on Earth).

From a ‘zoomed-out’ view, the main terrestrially-relevant areas of Space capabilities can be broadly bucketed as follows:

- Geospatial Intelligence: I want to sense what is happening somewhere else.

- Communications: I want to transmit data a great distance quickly and securely.

- Spatial Positioning: I need to know precisely where something is and when it is there.

- Transfer of Technology: I have an application in mind that needs or provides a high-performance capability or exhibits a unique property.

There are concentric rings across each set of capabilities to delineate the level of Space knowledge and organizational commitment necessary to extract value from any particular capability. The levels are:

- Product-Service: receiving decision-making information derived from Space assets.

- Data: Accessing raw data from Space that needs further processing by machines (and occasionally by Earthlings) before it is useful for a business.

- Asset: Owning, operating, and/or otherwise controlling an instrument, sensor, or other form of Space-based tool or system.

Below is a deeper look at the buckets of Geospatial Intelligence, Communications, Spatial Positioning, and Transfer of Technology, followed by an elaboration of the levels of capability (Product-Services, Data, and Asset) that applies to all buckets.

- Geospatial Intelligence (GeoInt) encompasses the means for imaging, scanning, and sensing of phenomena above, on, and below the Earth’s surface. Such instrumentation can be as specific as counting cars in a parking lot, identifying the presence of ancient buried ruins, or broader uses such as tracking the layers of a weather system that could develop into a hurricane. If you ever used Google Earth or the Satellite view in an app that gives driving directions, you were using GeoInt-derived data. The infrastructure necessary to enable GeoInt include imaging satellites, machine vision computing resources, and data downlink between a satellite and a ground station. Some common units of measure include the data’s resolution, which is often in square-meters (m^2), expanse as per square-kilometer, but at the Product-Service level there can be a variety of ways a business may engage, such as dollars-per-square-kilometer or cost-per-”insight”.

- **Communications (Comms) **is focused on how data is transferred as x-to-sat, sat-to-x, and sat-to-sat. This has to do with the uplink and downlink between an orbiting satellite or vehicle and a ground station located somewhere on Earth. For example, SpaceX Starlink is projected to have tens of thousands of orbiting smallsats, dozens or hundreds of ground stations on the surface, and thousands of end-user terminals (with consumer-friendly names like Dishy McFlatface). With mathematical choreography, they are able to send data bidirectionally between ground stations and terminals by relaying across whichever satellites happen to be passing overhead at the time of data transmission. Units of measure of satellite communications tends to be assessed similarly as terrestrial broadband measurements, such as gigabits or terabits per second. Satellite communications can occur via a variety of physical phenomena, such as radio frequency or optical (usually laser) means.

- Spatial Positioning (SPS) is for locating where things are, whether physical objects and entities or abstractions such as political borders. Underlying infrastructure include the Global Positioning System (GPS), a U.S.-origin service [2] comprising a constellation of satellites to emit radio frequencies at specific timed intervals that are detectable and interpretable by a GPS receiver, such as a mobile device, including most modern phones. Working in conjunction with terrestrial cellular towers, Wi-Fi nodes, and other telecommunications equipment, GPS is what allows a ‘you are here’ dot to appear on a map when you use an iPhone to get walking directions toward the nearest grocery store. With emerging applications in augmented reality, Spatial Positioning is becoming a crucial component of businesses. Historical applications are varied, including the use of detailed mapping that urban planners and self-driving vehicles are relying upon. The global hide-and-seek game Geocaching, as well as Niantic’s Pokemon Go, are consumer-grade examples of Spatial Positioning infrastructure being profitably leveraged for enjoyment by Earthlings.

video: Geo-located by the green dot. Screenshot by JMill with iOS. Animation by JMill.

- Transfer of Technology (ToT) is the development of new capabilities in one field that are then able to be refined and deployed in a different field or domain. This is often an endeavor reserved for organizations with R&D capabilities, to be able to effectively utilize technologies that were originally developed with Space in mind, but which may advance terrestrial capabilities in some way. The predominant ToT work occurs in the realm of atoms-based concerns, such as novel materials, lower friction mechanisms, new forms of automation, and greater tenability. For example, velcro straps were originally developed for securing objects to each other in low-gravity environments, but found utility for securing shoes to an Earthling child’s feet, among many other applications. There are also ToT opportunities in the digital realm, such as in the discovery and deployment of improved command and control architectures, data compression, and signal processing and error correction, to name a few areas. Companies developing undersea applications may benefit from Space technologies and vice-versa, particularly for GPS-denied navigation and autonomous decision making.

For deeper dives on several elements within the buckets of Geospatial Intelligence, Spatial Positioning, and Communications, check out Space Capital’s playbooks and companion resources for great starting points.

As the SPACE chart introduced earlier shows, there are multiple levels of organizational commitment that underpin the buckets of GeoInt, Comms, SPS, and ToT. These are Product-Service, Data, and Asset, elaborated as follows:

- Product-Service provide customers with insights, often information that its suitable for decision-making. For example, an industrial agricultural customer may pay for a map showing where particular soils are under-utilized and what to do about it. The purchase of Product-Services is the simplest point of engagement for Earthling businesses. Space-based Product-Service providers are proliferating as orbital capabilities improve and as traditional enterprises and markets become attuned to Space offerings.

- Data provides customers with a raw or lightly-cleaned stream of images, signals, blips and bloops, upon which the customer must have the means to further process the data into something more useful to the business. Carrying on the example introduced above of the agricultural customer, this would be as if the customer is receiving hyper-spectral times-series images and assessing them manually or, for more sophisticated customers, using the images as input into a proprietary vision computing tool. Consuming raw data streams is not common among most Earthling businesses due to the collateral needs for expertise, computing, and other resources to conduct effective data analysis, but it can provide a competitive advantage for prepared organizations.

- Asset provides customers with the ‘closest to the metal’ experience, involving some form of direct control and/or responsibility towardSpace-based hardware, like an imaging satellite. For our agricultural customer, this is akin to making a big commitment on the organization and its reliance on Space, such as by partnering with a satellite architect like Airbus Space and Defense to design and eventually operate a satellite (or at least a payload), strategize on orbiting needs, securing launch plans, planning end-of-life, etc. This is not for the faint of heart, as it is typically more expensive in the short and medium term compared to securing Data-level or Product-Service-level access. However, developing an Asset can be a strategic boon if done well. John Deere, best known for its agricultural equipment, has secured Asset-level access to Space, which may enable the company to develop new Product-Services. In a partnership with SpaceX, the company is connecting its equipment to high-speed Internet, an infrastructure play that reinforces the importance of the Agriculture industry to the Space industry, and vice-versa. See this Wall Street Journal article🚩 for more about the partnership.

The SPACE chart is intended to simplify – without dumbing down – several of the major areas where Space infrastructure will influence organizations. Some influence may be subtle, an astronomer’s society witnessing a string of smallsats heading toward their destination orbits.

Others are more pronounced, such as how we tend to rely on Uber to ferry us via optimal route to a new restaurant on the other side of town that we saw pop up on Yelp – both Uber, Yelp, and thousands of other companies couldn’t have emerged without Space-based assets quietly operating behind the scenes. You may be surprised at the sheer number of employees – perhaps a third or greater – at these companies whose jobs are focused on improving geospatial accuracy to improve user experience and business outcomes.

[1] The analogies above are based on a conversation between Delian Asparouhov and Jason Calacanison This Week in Startups episode 1793.

[2] There are efforts among other nations to build GPS-equivalent systems as a priority for national sovereignty.

Applications

Space for Earth and Earth for Space

Space for Earth and Earth for Space

It has long been a point of advocacy for organizations such as NASA to justify its Space ambitions as benefitting Earthlings through the development of new technologies, from camera phones to ‘astronaut ice cream’. It is unsurprising that NASA’s Technology Transfer Program (TTP) is the Agency’s longest continually operated program. Space Technology Directorate Associate Administrator James L. Reuter stated:

“One partner invented a laser a fraction of the size of any comparable laser, which can now analyze Earth’s atmosphere, improve glaucoma treatment in developing countries, and more. The 2020 [Mars] rover carried the first aircraft (a helicopter, in fact) to fly in Mars’ thin atmosphere. The company that built the craft’s rotors and other components, which has worked with NASA on multiple previous aircraft, applied its Mars-honed expertise in the creation of a commercial drone that’s now helping farmers monitor their crops.”

Earth → Space: terrestrial companies entering the Space economy

Savvy Earthlings leading terrestrial companies may uncover opportunities to tailor their existing services to the burgeoning Space sector. The flow is not one-way. Just as Space technologies seed terrestrial applications, companies with deep terrestrial expertise are finding that their capabilities are directly valuable in orbit.

SpiderOak for years has provided data backup services with best-in-class security to enterprises, small businesses, and consumers. The company expanded its product-service offerings oriented to organizations managing Space assets. When satellites need end-to-end encrypted data storage, the cybersecurity principles are the same whether the server is in a data center or in orbit.

Dotphoton is a team of image compression experts who developed software for reducing the filesizes of hefty RAW photographs taken by common DSLR cameras. Among the world’s experts in preserving image data while reducing the overall data payload, the team’s sophisticated noise filtering and sensor characterization turns out to be effective for Space-based imaging services. (Dotphoton and the European Space Agency began a partnership in 2022.)

Apple’s partnership with Globalstar may be the most consequential example of a terrestrial giant entering Space infrastructure. Apple has invested over $1.7 billion in Globalstar’s satellite network, funding 95% of the costs for a new generation of satellites. 1 The result: emergency SOS, messaging, and Find My services via satellite, available to hundreds of millions of iPhone users globally. When Space becomes invisible to the end user, when you don’t even know you’re using a satellite, that is the mark of true technology transfer.

There will be growth opportunities in supporting orbital data streams, particularly how Space-based assets are increasingly Internet-connected. The question for every Earthling business leader is not whether Space technologies will reach your industry, but whether you will be the one adopting them — or the one being disrupted by a competitor who did.

- ↩︎

Apple committed $1.7 billion to Globalstar in 2024 for satellite iPhone services. Globalstar allocates 85% of its network capacity to Apple, which accounts for 63% of Globalstar’s revenue.

Applications

Tunable gravity

Tunable gravity

If gravity could be changed with the twist of a knob, what would you do with it? This rhetorical question has historically been only hypothetical for nearly all of us outside of certain scientific research communities. However, orbiting platforms and small satellites are providing new capabilities for in-space testing and manufacturing in sustained microgravity (“low-G”) and no-gravity (“zero-G”) environments. No longer must a research team exploit an airplane’s parabolic flight for a brief thirty-second low-gravity ‘window of opportunity’ afforded by specialty companies such as Zero-G. You can book your own flight, but for the rest of us landlubbers, we can daydream by watching how music group OK GO produced the video for one of their hit songs.

“No one knows how organisms respond to other levels of gravity,” stated Marybeth Edeen, ISS Research Integration Office Manager at Johnson Space Center, in NASA’s Spinoff publication. Biological processes may behave differently at different gravities, the study of which is anticipated to have favorable implications on pharmacology, materials development, electronics fabrication, and a variety of other fields. For example, an improved hepatitis C treatment explored by Schering-Plough Research Institute was developed by forming better protein crystal structures in a weightless environment. The result was a protein structure that was better targeted at hep-C while curtailing side effects.

Academic and corporate experiments conducted aboard the International Space Station using Techshot’s Multi-Use Variable-Gravity Platform (MVP), which simulates any level gravity between weightlessness and twice Earth’s gravity (“2 G”), is one key tool among others including bioprinters for producing organs from stem cells, zero-G deposition printing of metals and electronics. Varda Space Industries is building in-space manufacturing capabilities with early interest among pharmaceutical companies. Space Tango is among a cohort of organizations that are exploring the commercial opportunities enabled by viewing gravity as a variable rather than a constant. One of Space Tango’s customers, LambdaVision, is developing retinal implants requiring thin, even layers so recipient patients can gain restored sight. Earth’s gravity makes the layers settle unevenly, so, despite the cost penalty of orbital launch and recovery, “The goal … is to test out the new automated process to produce the implants on a commercial scale,” states Space Tango founder Twyman Clements. “Space is really a means to an end, and so we use space to create these things, retinal implants, fiber-optic cables, for the benefit of Earth.” 2

The factories are flying

Since this article was originally published in early 2024, the pace of orbital manufacturing has accelerated dramatically.

Varda Space Industries has become the commercial leader in orbital manufacturing. The company completed its first successful reëntry capsule mission (W-1) in February 2024, manufacturing ritonavir, an HIV/Hepatitis C antiviral, in its metastable Form III crystal structure, a polymorph that is difficult to produce under Earth’s gravity. 3 Varda has since completed four capsule missions (W-1 through W-4), with W-4 being the first to fly on a Varda-built satellite bus rather than a Rocket Lab Photon. The company raised $187 million in a Series C round in mid-2025, bringing total funding to approximately $329 million. 4 No FDA approval has been granted yet for a space-manufactured drug, but the regulatory pathway is being charted, and the technical feasibility is no longer in question.

Redwire returned the first bioprinted cardiac tissue from the ISS in May 2024, printed from a single human donor’s cells. The company had earlier produced the first human knee meniscus bioprinted in orbit. In March 2025, the ISS produced its first metal parts using ESA’s Metal 3D Printer. Redwire’s 2025 revenue reached $335 million with a record backlog of $411 million — the orbital manufacturing sector has real revenue, not just R&D grants. 5

For Earthling business leaders, the strategic insight is this: if your industry involves crystal growth, protein folding, fiber drawing, bioprinting, or any process where gravitational settling, convection, or sedimentation limits quality, then microgravity is no longer a curiosity. It is a production environment. The cost premium of orbital manufacturing will decrease as launch costs continue to fall (see Is Space just cool, cold, and costly?), and the companies that have already characterized their processes in microgravity will be first to market when the economics tip.

- ↩︎

As quoted in NASA’s Spinoff publication.

- ↩︎

Varda Space Industries W-1 mission: launched June 2023, returned February 21, 2024. Varda became the third corporate entity to return cargo from orbit (after SpaceX and Boeing). The ritonavir Form III polymorph survived reëntry intact, per analysis published on ChemRxiv.

- ↩︎

Varda raised a $187 million Series C in July 2025, led by Natural Capital and Shrug Capital, bringing total funding to approximately $329 million.

- ↩︎

Redwire reported full-year 2025 revenue of $335.4 million (+10.3% YoY) with a record backlog of $411.2 million.

- ↩︎

Flawless Photonics (formerly Flawless Space Fibers) launched on NG-20 in January 2024 and produced over 11.9 km of ZBLAN in two weeks aboard the ISS, with seven draws exceeding 700 meters each.

- ↩︎

Axiom Space revised its assembly sequence, targeting free-flying station status as early as 2028. The first module’s pressure vessel was completed in 2025 and is built by Thales Alenia Space.

Strategy

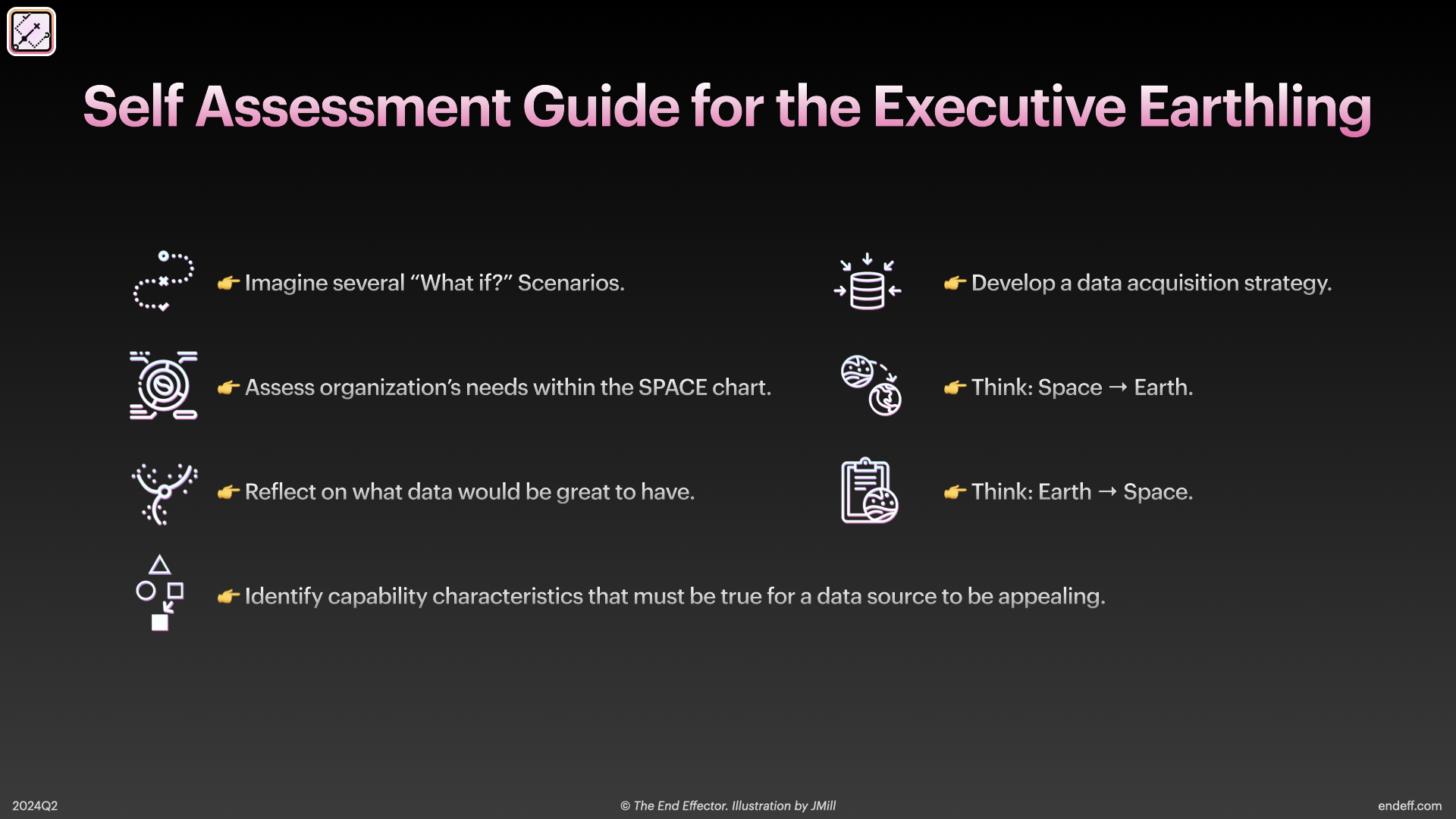

Self Assessment Guide for the Executive Earthling

Self Assessment Guide for the Executive Earthling

This is a guide that a business leader can utilize to evaluate how the organization can become Space-informed. It can be useful for an interdisciplinary team to work on independently to share findings, identify unknowns, and establish an organizational learning agenda. This can underpin the development of a plan so the organization has specific individuals who are directly responsible for tracking developments and engaging with prospective collaborators.

Step 1: Imagine several “What if?” scenarios

What are all the physical assets your organization should track? What if you could know where all of them are in real-time? What if your competitor also knew where all of your assets were? Suppose your organization is scouting new site locations. What if you could anticipate which prospective sites would be denied property insurance due to insurers’ climate-informed policy changes? What if your organization’s engineering team could identify and incorporate, at comparatively low cost, Space-derived technology?

The “What if?” exercise is not about science fiction — it is about identifying the information gaps your organization lives with every day and asking whether orbital data sources could close them. A logistics company might ask: “What if we could see real-time road conditions at every point on our routes?” A mining company: “What if we could detect subsurface mineral deposits before breaking ground?” An insurance company: “What if we could re-price policies weekly based on satellite-observed climate indicators?”

Step 2: Assess your organization’s needs within the SPACE chart

Map your organization’s interests against the SPACE chart framework, across the four domains (GeoInt, Comms, SPS, ToT) and three levels (Product-Service, Data, Asset). This exercise aids in identifying which areas to direct attention for your organization in order to track new developments and collaborations. Most organizations will find they are already consumers of Space-derived Product-Services (GPS navigation, weather forecasts) without recognizing them as such.

Step 3: Reflect on what data would be great to have

If there are particular characteristics you would want to know about any location on Earth, what would they be? Soil moisture, building occupancy, mineral presence, energy generation, micro-weather patterns, or the contents of illegal dumping. Framing the question as “What would we do if we had perfect information about ___?” reveals the highest-value data opportunities. Then ask whether any Space-based data provider already offers something close. You may be surprised.

Step 4: Identify capability characteristics that must be true for a data source to be appealing

For now, deprioritize price point. What is the minimum viable and nice-to-have data cadence? What happens if you get a new batch of data once an hour versus once a year? How does it impact your organization? How would you invest resources differently? A farm needs soil data weekly during growing season. A shipping company needs port imagery daily. A financial services firm wants retail foot traffic data hourly. The cadence requirement shapes which level of the SPACE chart (Product-Service vs. Data vs. Asset) makes economic sense.

Step 5: Develop a data acquisition strategy

Assess how your organization can achieve holistic data collection and decision-making. Space-borne data is just one form; how does it complement other forms such as from humans in aircraft, humans on the ground, autonomous drones, and other sources? How can you prepare your organization to ingest multi-modal data sources to make better-informed and better-timed decisions? The most sophisticated organizations (think Maersk optimizing global shipping routes or John Deere connecting farm equipment via Starlink) don’t use Space data in isolation. They layer it with ground sensors, IoT devices, and AI-driven analytics.

Step 6: Think Space → Earth

Review intellectual property portfolios from NASA’s Technology Transfer Program, the top provider of such licensable technologies. Licensing a patent can be the start of a long-lead research and development endeavor, but can provide standout performance for the licensing entity as it gets novel product-services to market based on space-derived underlying technologies. See Space for Earth and Earth for Space for specific examples of companies that have already done this successfully.

Step 7: Think Earth → Space

Proactively engage with Space players to problem-solve, generate ideas, and to understand where they are experiencing bottlenecks in communication throughput, compute, sensing reach, and partnerships. There can be fruitful relationships built around new lines of business and capabilities that are increasingly shareable as Space systems become less ‘boutique’ in their designs and can benefit by adopting interoperation standards and terrestrial-grade hardware. Companies like SpiderOak and Dotphoton began as purely terrestrial businesses and found that their expertise was exactly what the Space industry needed.

Once you have worked through all seven steps, you will have a clearer picture of your organization’s Space readiness and a concrete learning agenda for what to track next. For the economic context behind these decisions, continue to Is Space just cool, cold, and costly?.

Strategy

Is Space just cool, cold, and costly?

Is Space just cool, cold, and costly?

Space is ‘cool’. The proliferation of NASA-branded swag, space-themed science-fiction media, and adulation of Space-faring heroes such as the Apollo Mission teams shows the general public’s overall appetite for thinking about Space. (This is a typical U.S.-centric perspective.) Space has indeed maintained a ‘coolness’ factor for decades, if not millennia: as Scarlett Koller of Mithril Technologies stated when I interviewed her on Tough Tech Today, “I actually think it’s very human, really there isn’t a culture that we know of that hasn’t named the stars that they could see.”

In regard to marketable selling points, enhancing brand reputation through Space involvement might not resonate with all stakeholders, as some might view it as an unnecessary diversion from core business operations. It could be argued that BP’s involvement in space solar power projects does not mitigate the environmental impact of its oil and gas business, nor is Budweiser’s “space beer” more than a marketing piece.

Space is cold. Most of us know that Space is literally mostly a frozen, desolate vacuum, interspersed with blazing hot balls of rock and gas every few parsecs, plus or minus a lightyear. Our cozy part of the universe is anomalous (but it is not the only), and most everywhere else is a brutal environment that is challenging for even our species’ best autonomous robots.

Space is also costly – but unit economics are changing favorably. The public had been trained for a half-century that Space is for nation-states and unlimited budgets. In the late 2000s and early 2010s, that perception began to evolve as several billionaires, including Elon Musk, Jeff Bezos, and Richard Branson, poured their personal wealth into launch services. However, in the 2020s, we see a clear transition to venture capital investment. As Ashlee Vance, author of When the Heavens Went On Sale notes, “Trying out an idea in space no longer requires congressional approval or some wild-eyed dreamer willing to risk his personal fortunes; it just requires a couple of people in a room agreeing that they’re willing to spend someone else’s money on a huge risk.”(*When the Heavens Went On Sale *by Vance. HarperCollins. 2023. Page 17.) “In 2021, private capital more money in the space industry than **NASA **will spend on everything,” statedShanti Rao, NASA-JPL physicist and startup investor, and based on data sourced from Space Capital’s industry reporting.

Lets focus more on costs, since there are several and each is a key consideration for senior business leaders.

A drop in launching cost spurs an increase in launch

What happens when it costs less to launch goods around the planet on a SpaceX Starship rocket compared to the status quo of airlifting via a Lockheed Martin KC-130 cargo plane? As the cost to launch a heavy object into LEO has decreased by several orders of magnitude, it has implications not only on how much ‘stuff’ we can launch to Space, but what also can return back to Earth. It cost roughly $54,500 per kilogram to ride the U.S. Space Shuttle, approximately $1,500 per kilogram on SpaceX’s Falcon Heavy, and Starship (which completed 11 integrated flight tests through late 2025) is projected to achieve a price point under $100 per kilogram with reuse. 8 Launch cost is an important instigator of space development in much the way that low-cost access to large bodies of water such as navigable rivers helped port cities to grow on the top of lowered transportation costs. (For a deeper look at this, check out Tomas Pueyo’s thread.)

Hidden costs of orbiting data streams

GeoInt, specifically Earth Observation, is among the fastest growing segments serving terrestrial businesses like financial services, mining, logistics, et cetera. Companies providing capabilities for earth sensing tend to focus on the cost of data. While important, it is not the only cost for which terrestrial leaders must account.

When pricing a Space-origin data stream, Earthlings should probe:

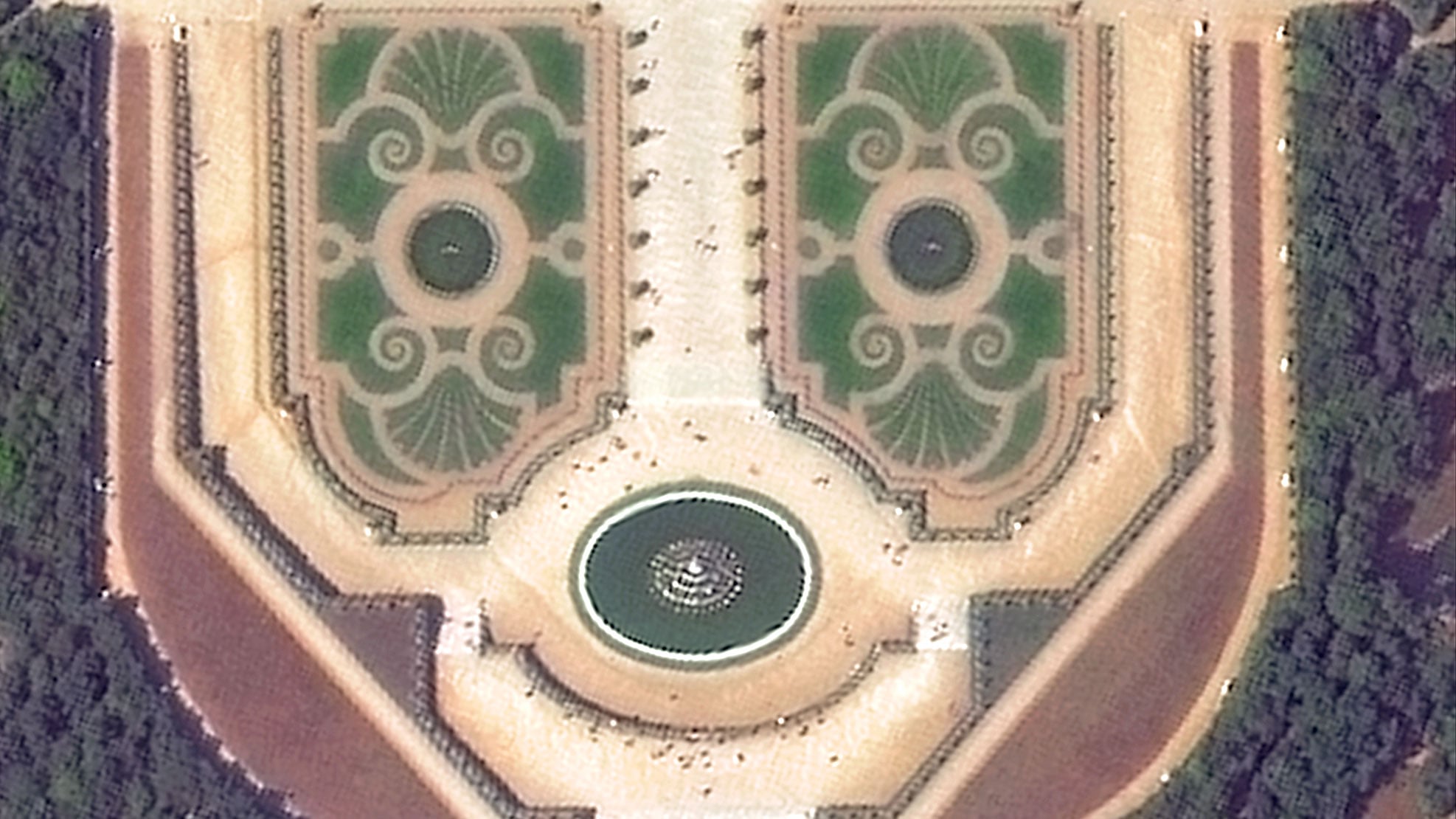

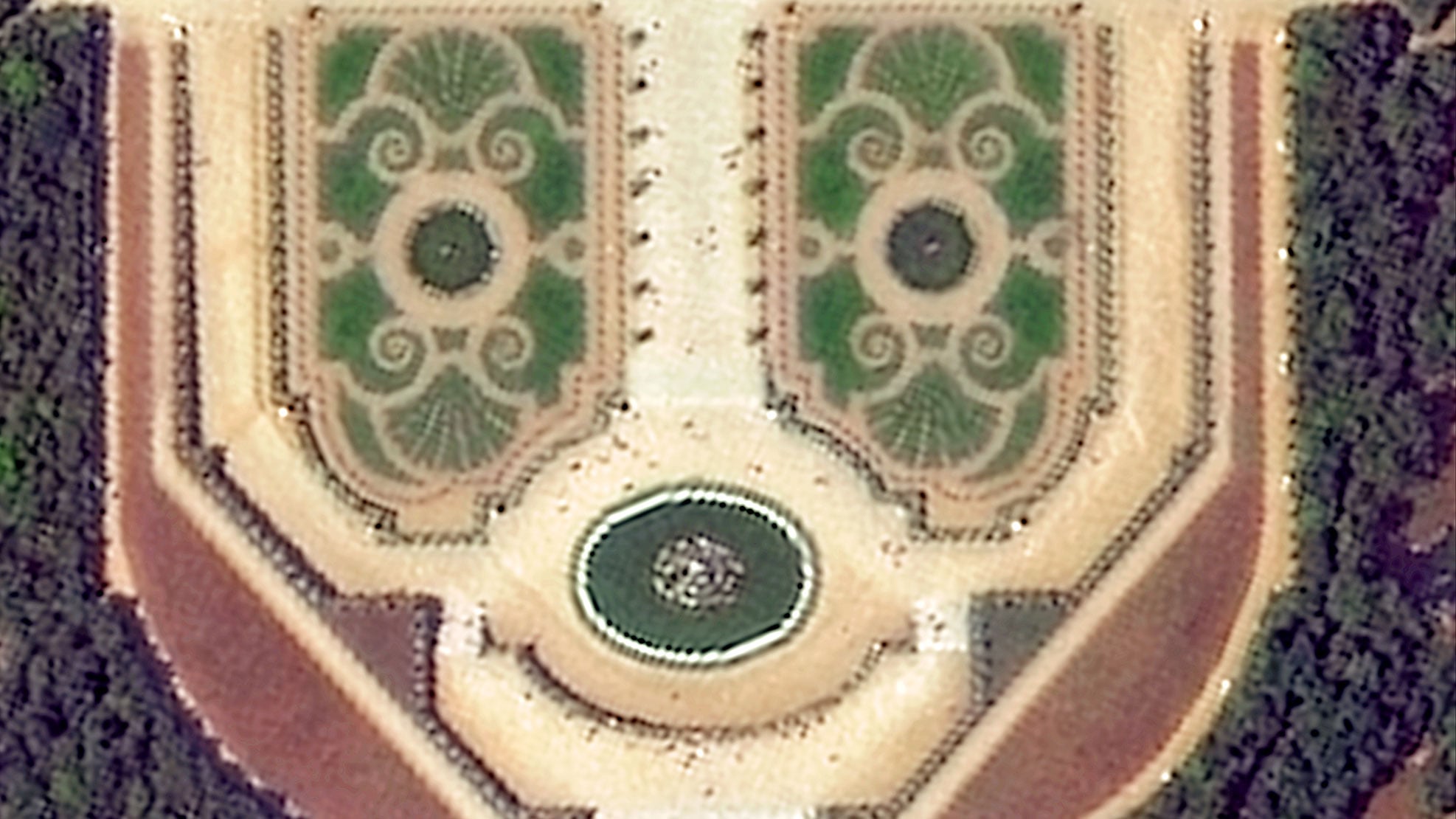

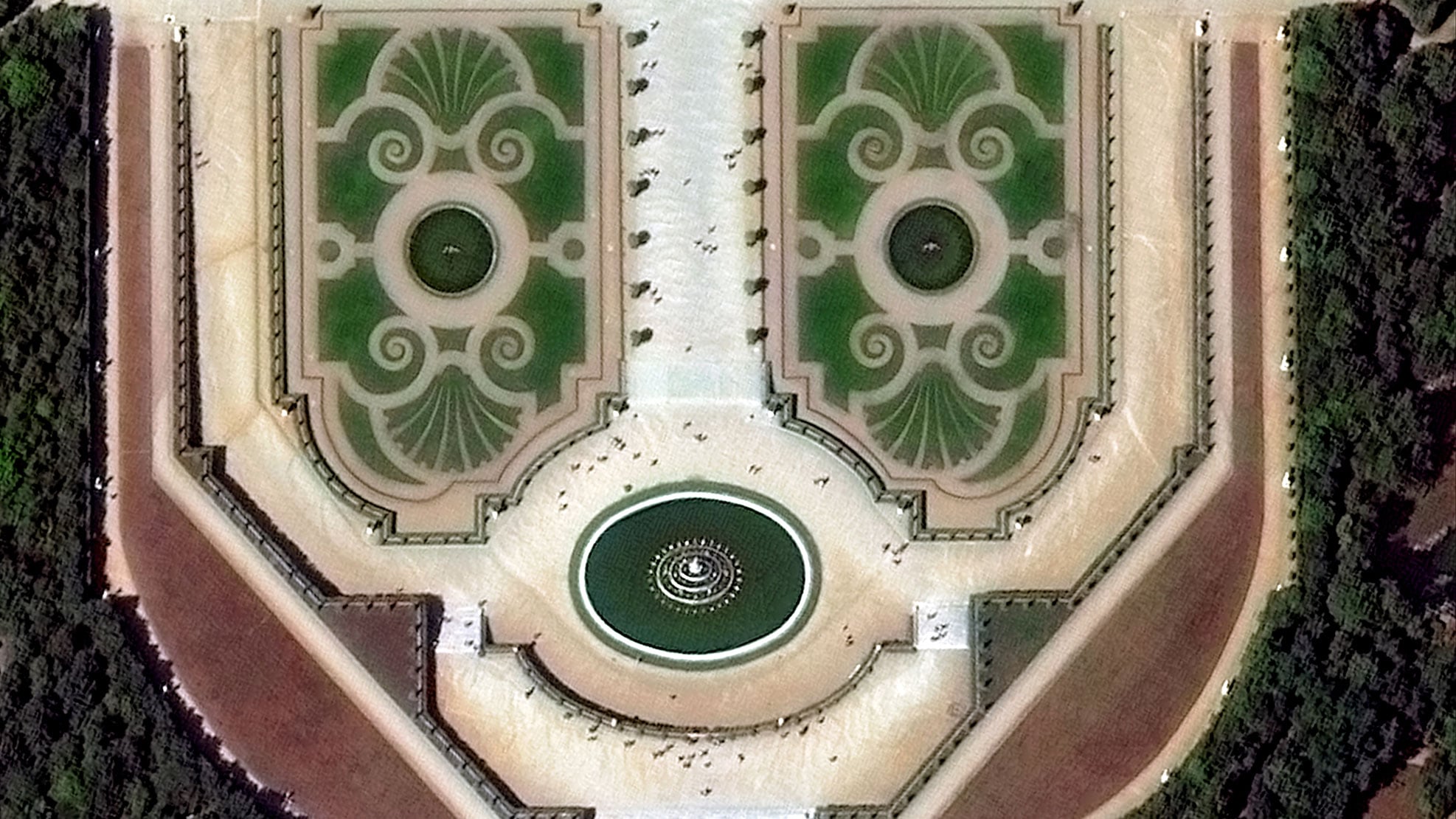

- Cost of data. This would be the dollar-per-square-kilometer cost for a multispectral image. Planet Labs, an early provider of imagery data, provides subscription services including daily global coverage at a resolution of multiple meters per image pixel and rapid taskable imagery that is a higher resolution of deca-centimeters per image pixel. See below for a visual comparison provided by Maxar of differing image resolutions.

Satellite images from Maxar. Drag the slider to compare resolutions of the palace at Versailles. Note the quality of detail, including of individual people walking about.

- Cost of compute. Once a dataset has been retrieved, there are often large computational needs to analyze the data for whatever the organization cares about. For example, it is common to want to look for new or anomalous objects, or to count or measure certain objects while ignoring others. Machines are great for this task, but powering these processing systems often requires dedicated and tuned computational infrastructure. The Utilis company may provide a plot of water leak locations to utility managers once a quarter or twice a year.

- Cost of human resources. If ‘off-the-shelf’ products are unavailable but an Earthling organization really wants a particular capability, the development must occur in-house or through partnership. Both approaches require redirecting internal human resources and, likely, increasing hiring for Space specialists. This is typically a very expensive and strategic endeavor before any return on investment could be recouped.

- Cost of change. An organization’s cultural norms can make it difficult to strategically evolve the organization into a new market position. While value-based evaluation of if and how to incorporate Space capabilities into the organization is probably the best metric from a shareholder’s perspective, from the perspective of the rank-and-file employees there can be expected skepticism and reluctance toward such a shift.

Beware revenue model (mis)alignment. The Space industry mostly runs on a project-based model with customers paying for Earth Observation capabilities on-demand, which is usually when no other option remains for the customer. Earth observation is often priced per square kilometer or “per scene”. This does not scale well when an organization needs to construct a time-series analysis over a wide-spanning area. A better alignment of incentives is to provide a subscription model with customers relying on space-based resources on a recurring basis, which makes the capability strategic to the (non-Space) organizations. For most companies, the adoption of geospatial data is not an inevitability. Having the technology available does not make it ready to be adopted. As stated by Aravind Ravichandran of TerraWatch Space, a consulting firm focused on earth observation applications, “The adoption chasm is real – as weird as it sounds, launching satellites and beaming the data down does not seem like the hardest bit. …It is super important to compare the relative benefits of what we bring to the table instead of just offering something that is ‘cool’ because data comes from space!” Noted earlier, there can be a cost to change, which can manifest as employee reluctance to adopt what an organization has strategically identified as a good value investment in Space capability. When a new Space initiative is financially modeled and shows opportunities to “free up a lot of time and that person can now go and do something else or so the productivity of the person improves,” Ravichandran of TerraWatch described to me, “that’s more of an organization perspective” rather than accounting for concerns from an employee’s point-of-view.

Just because the data is Space-origin doesn’t make it the best or defensible for a business. For some forms of earth observation, sometimes it is easier (and lower cost) to simply hire a human to fly an airplane overhead or to contract someone to stand on a street corner and count cars. As a case example on this approach, see the Radiolab episode Eye in the Sky* *for a story on tracking crimes with airplanes. Here is an excerpt: “In 2004, when casualties in Iraq were rising due to roadside bombs, Ross McNutt and his team came up with an idea. With a small plane and a 44 mega-pixel camera, they figured out how to watch an entire city all at once, all day long. Whenever a bomb detonated, they could zoom onto that spot and then, because this eye in the sky had been there all along, they could scroll back in time and see – literally see – who planted it.”

Thus, persistent surveillance is feasible with satellite systems but also with other modalities. See this Washington Post article🚩 for an example. Companies like Fraym offer services to synthesize multi-modal approaches so that their customers can avoid mucking through this form of data analysis.

Earth observation data sets costs a lot if one wants to monitor a large area often. Pricing is usually dollars-per-square-kilometer. The surveying cadence matters, as costs grow quickly if an organization needs hourly or daily snapshots rather than monthly or quarterly. As the headline of a 2022 piece by BCG states, “Satellites Are the Next Frontier for Industrial Companies”, though the piece was not intended to delve substantively into the nuanced cost characteristics of such data sources. Data sources that are newer, smaller, more numerous and more expendable in LEO and MEO are reducing the cost curve compared to GEO systems.

- ↩︎

Launch cost data: Space Shuttle ~$54,500/kg; Falcon Heavy ~$1,400-$1,500/kg; Starship projected at ~$78-$100/kg with partial reuse, with a long-term goal of $10-$20/kg at high reuse rates. Starship completed 11 integrated flight tests through October 2025, including the first successful payload (Starlink simulators) deployment on IFT-10. Sources: NASA historical data, SpaceX published figures, analyst estimates.

Case Studies

Mining, the most 'terrestrial' sector, is changing due to Space

Mining, the most 'terrestrial' sector, is changing due to Space

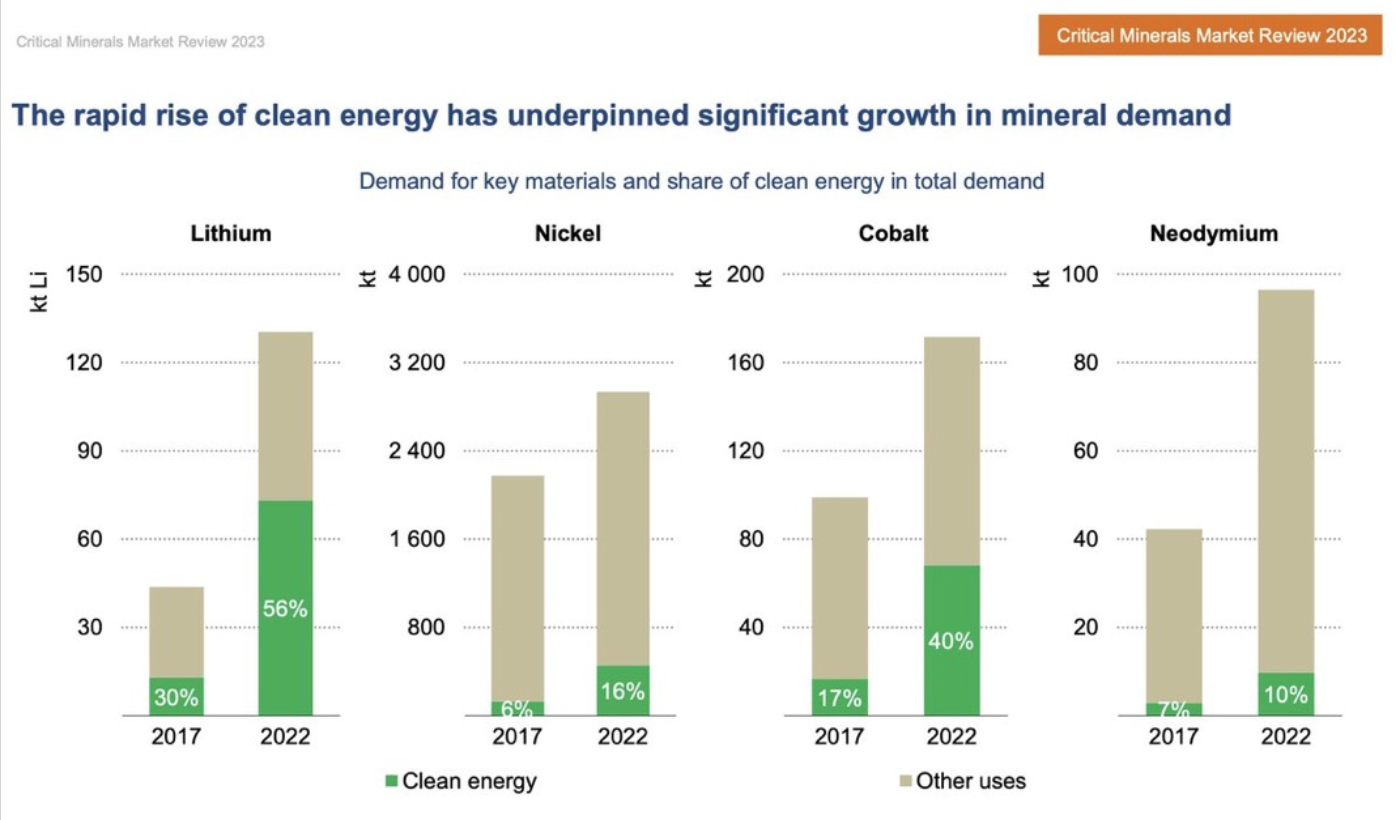

The miner’s credo is “If you can’t grow it, you have to mine it.” The transition towards clean energy has led to a significant rise in demand for critical minerals. As part of a burgeoning Earth observation strategy, SAR is beginning to be utilized by certain mining companies to find particular minerals, such as lithium.

Geospatial data, especially from multispectral, hyperspectral, and SAR sensors for Earth observation, has a significant role to play in the mining technology stack, across applications, from exploration to risk management. The IEA’s Global Critical Minerals Outlook 2025 paints a stark picture: lithium demand grew approximately 30% in 2024, with the energy sector driving 85% of total demand growth for battery metals. Looking ahead, the IEA projects lithium demand to grow fivefold and nickel/graphite to double by 2040. 9 Perhaps most concerning: the average market share of the top three producers for key minerals rose to 86% in 2024, with nearly all supply growth concentrated in China and Indonesia. 10 The mining sector will rely on staggering amounts of EO data if the Space industry is able to offer reliable, scalable, and commercially viable product-services.

Japan Aerospace Exploration Agency’s (JAXA’s) Hayabusa and Hayabusa 2 spacecrafts successfully returned to Earth asteroid samples in 2020 and 2022, helping the Space industry to learn about the challenges and opportunities of safely recovering materials not resident on Earth. NASA’s OSIRIS-REx returned an asteroid sample in 2023 — 70.3 grams from asteroid Bennu, containing minerals that hint the asteroid may have splintered from an ancient ocean world. 11

Commercial asteroid mining remains in its early stages but is advancing. AstroForge became the first private company to send a spacecraft toward an asteroid in deep space with its 2025 Odin mission, though the spacecraft was lost due to ground station failures. The company’s third mission, Vestri, is planned for 2026 and aims to dock with a metallic near-Earth asteroid and measure its composition for future extraction. 12 Meanwhile, Lunar Outpost (disclosure: the author is a shareholder) has scored major milestones: its MAPP rover became the first U.S. commercial rover to reach the lunar surface in early 2025, and the company was selected for the Artemis IV mission in December 2025. Lunar Outpost also leads the Lunar Dawn team, alongside GM and Goodyear, which was awarded NASA’s Lunar Terrain Vehicle contract with a potential value of $4.6 billion. 13

Testbed facilities such as those operated by Swamp Works at NASA and the Center for Space Resources at the Colorado School of Mines provide simulated regolith-strewn physical environments for companies to refine their mineral exploration and excavation rovers before heading to their harsh primetime site targets on the Moon and Mars.

- ↩︎

IEA Global Critical Minerals Outlook 2025: lithium demand up ~30% in 2024; projections show 5x growth for lithium and 2x for nickel/graphite by 2040. Energy sector accounted for 85% of total demand growth for battery metals.

- ↩︎

IEA 2025: average market share of top 3 producers for key minerals rose to 86% in 2024 (from 82% in 2020). The IEA’s N-1 analysis shows that if the largest single supplier is disrupted, remaining graphite and rare earth supply covers only 35-40% of projected 2035 demand.

- ↩︎

NASA’s OSIRIS-REx returned 70.3 grams from asteroid Bennu in September 2023. Analysis published in January 2025 confirmed 14 of 20 protein-building amino acids, all 5 DNA/RNA nucleobases, and magnesium-sodium phosphate of unprecedented purity. The sample contained an equal mixture of left- and right-handed amino acids, suggesting chirality selection happened after asteroid material seeded early Earth.

- ↩︎

AstroForge became the first private company to send a spacecraft toward an asteroid in deep space with its February 2025 Odin mission. The spacecraft was lost in March 2025 due to ground station failures. The company has raised approximately $60 million and plans its third mission (Vestri) for 2026 to dock with target asteroid 2022 OB5.

- ↩︎

Lunar Outpost’s MAPP rover reached the lunar surface in the March 2025 Lunar Voyage 1 mission. In April 2024, the Lunar Dawn consortium was awarded NASA’s Lunar Terrain Vehicle Services contract (potential value $4.6 billion). In December 2025, MAPP was selected for the Artemis IV mission.

Case Studies

Reasons why an everyday Earthling could ignore Space

Reasons why an everyday Earthling could ignore Space

Every thesis deserves a devil’s advocate. If you have read the preceding articles and still harbor skepticism about whether Space matters to your organization, this article takes your objections seriously — and then stress-tests them.

Is growth of the Space industry overhyped, the market saturating, and returns diminishing for new entrants? Proponents of this argument may point to the dot-com bubble in the early 2000s, which saw many Internet companies fail as the market became oversaturated. While the space industry may face saturation, businesses can focus on niche markets and applications to mitigate risks and maximize returns. Planet Labs specializes in high-resolution Earth imaging and successfully serves a niche market within the broader satellite industry.

Might the adoption of space-derived technology lead to high research and development costs with uncertain returns on investment? There are emerging technologies that may not prove commercially viable. The Concorde supersonic jet was a technological marvel, but high development and operational costs made it commercially unsustainable, despite being in service for nearly three decades. While Concorde investors have long ago taken their losses and soured the aviation industry toward supersonics, there is a new generation of low-boom craft that might become financially tenable. The NASA Quesst program has the mission to provide sufficient data to rewrite aviation regulations to permit overland supersonic operation.

Companies can leverage partnerships and government programs to minimize R&D costs while maximizing the benefits of space-derived technology. Public-private partnerships are routinely utilized by Space entrepreneurs to partner with the U.S. government to develop goods and services based on existing research and technology development, along with grant support. The government provides resources and expertise through agencies that not only include NASA, but also the National Oceanic and Atmospheric Administration (NOAA), the Small Business Administration (SBA), and the Department of Energy (DOE). The Office of Space Commerce provides access points spanning the U.S. government.

Establishing a proprietary satellite communications asset is difficult for small organizations to afford. The high initial cost of deploying a satellite network can be prohibitive, limiting their ability to capitalize on satellite communications. However, as satellite technology continues to advance, costs are decreasing, making it more accessible and affordable for businesses of all sizes. The decreasing cost of launching CubeSats has enabled even small businesses and startups to access space-based communication services. Upstart companies such as Loft Orbital are catering to organizations by providing end-to-end satellite design, launch, and management services. If managing satellites is not an organization’s primary line of business, hiring Loft Orbital as a value-add Space liaison could generate a greater net present value for the customer organization while mitigating execution risk.

Could streamlining supply chains with Space-based solutions prove unnecessary and costly for companies with simpler, more efficient terrestrial options? Many local or regional businesses might find it more cost-effective to rely on existing ground-based logistics trackers and networks rather than invest in space-based technologies. While terrestrial options may suffice, the potential for global reach provided by space-based solutions can offer competitive advantages. For example, global shipping companies like Maersk utilize satellite-based navigation systems to optimize routes and reduce transit times, and Maersk has deployed Starlink across 330+ container ships for real-time fleet communications. 14

Environmental sustainability practices can leverage Earth observation data, but could the impact of satellite data be minimal since most businesses will struggle to translate this data into actionable strategies? Indeed, there are companies that might find it challenging to reconcile the vast amount of satellite data with their specific sustainability goals and mandates, leading to limited tangible results. This has been one of the biggest bottlenecks of the industry, but the logjam is loosening quickly. By collaborating with specialized data analysis companies, businesses can effectively utilize satellite data to inform and improve their sustainability practices. Descartes Labs uses artificial intelligence and satellite imagery to help businesses optimize usage of water and land, ensuring more sustainable practices.

If we invest in Space-focused workforce development, will this divert resources away from more immediate talent needs? It would be generally unwise for a company specializing in the automotive industry to prioritize investment in Space-related workforce development versus electrified powertrain technologies. However, if said company neglects to recognize the new capabilities that are coming online and changes to consumer expectations (some of which are instigated by or addressable with Space-based technologies), the company may find itself in a vulnerable position that trends toward becoming irrelevant among industry peers and new market entrants.

Engaging in strategic space collaborations could create financial and operational risks, as partnerships might not deliver the expected outcomes or could fail altogether. The partnership between Google and WorldVu Satellites dissolved in 2015 due to disagreements over project control. The company, later rebranded as OneWeb, went through bankruptcy in 2020 before being acquired and merged with Eutelsat in 2023, and now operates 633 LEO satellites serving aviation, maritime, and government customers globally. 16 Even failed partnerships can yield infrastructure that eventually finds its market.

Businesses can mitigate the risks of space collaborations by conducting thorough due diligence and choosing partners with aligned goals and values. For example, automotive original equipment manufacturers (OEMs) have begun establishing relationships with Space companies, such as Toyota’s work with Iona Space Systems to utilize satellite communications for navigation and autonomous driving.

The objections above are real, and any responsible business leader should weigh them carefully. But the pattern across every objection is the same: the risks of premature investment are concrete and measurable, while the risks of not paying attention are diffuse and easy to dismiss, until a competitor demonstrates what you missed. The Self Assessment Guide provides a structured way to evaluate which Space capabilities matter to your specific organization, and the SPACE chart helps you categorize them.

If you are evaluating whether your organization should invest in frontier technology more broadly, The End Effector’s Robotics CoreExplorer and Machine Intelligence CoreExplorer provide the same strategic depth across those domains. The pattern is consistent: the organizations that build informed perspectives early, even if they decide not to act immediately, are the ones that move fastest when the economics tip.

- ↩︎

Maersk has deployed Starlink across 330+ container ships. Starlink maritime installs are projected to reach approximately 130,000 vessels by 2026, with average revenue per vessel of approximately $34,000/year.

- ↩︎

Apple committed $1.7 billion to Globalstar in 2024 for satellite iPhone services, with Apple funding 95% of costs for a new generation of satellites. Globalstar allocates 85% of its network capacity to Apple.

- ↩︎

OneWeb went through Chapter 11 bankruptcy in March 2020, was acquired by a consortium including the UK government and Bharti Global, and completed its merger with Eutelsat in September 2023. The combined entity now operates 633 LEO satellites and has ordered 440 next-generation satellites from Airbus.

Space for Earthlings Acknowledgements, Contributions, and Disclosures

Changelog

v2.0.20260304 — Enhanced & Expanded edition: interactive SPACE Chart, Self-Assessment Tool, Launch Cost Explorer; enriched all articles with callouts, glossary terms, updated 2025-2026 data, and cross-references to Robotics and Machine Intelligence Cores

v1.1.20260224: streamlined articles; migrated to endeff.com; visual refresh

v1.0.20240315: public release

v0.9.20240115: soft release

Acknowledgements and Contributions

Thank you to Michael Cassidy, Scarlett Koller, Aravind Ravichandran, Mem Miller, Malvika Miller, and anonymous colleagues for your contributions. And thank you to the many subject matter experts over the years with whom I have had the pleasure of discussing the topics that inspired this series of articles.

Disclosures

The author owns shares in Lunar Outpost.

Stay informed

Ready to go deeper?

Space for Earthlings is just the beginning. The End Effector's Robotics Core, Machine Intelligence Core, quarterly Thrusts, and Telemetry newsletter give you the same depth across every frontier technology domain.